所在位置:首页 > 贸促动态 > 市长国际企业家顾问会议 > 往届回顾 > 第九届顾问报告 > 正文

Charting Beijing's future: The right balance of policies and qualities can push the city to the forefront

2012年05月23日 来源:中国国际贸易促进委员会北京市分会

What factors will vault Beijing to the very front ranks of the world's greatest cities? In one context, that isn't too far to travel considering Beijing's position at the heart of Chinese government, culture and history. Yet in another perspective, joining long-dominant world capitals of business, finance and culture like London, New York, Paris and Tokyo is a challenge that requires strong planning and concerted action.

Holistic planning for 21st Century cities

Fundamentally, the management of cities of the future will be a complex affair.

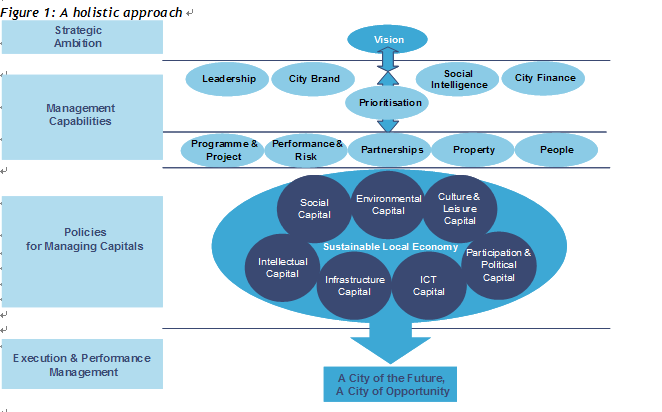

PricewaterhouseCoopers recommends adopting a holistic approach (see chart) to guide Beijing forward. This will allow leaders to steer the city ahead in balance with a range of economic, financial, social and cultural considerations.

The starting point for any city, even more so for Beijing with its potential for rapid growth, is formulating a clear vision that captures its strategic ambition. In order to channel all resources toward accomplishing the vision, Beijing's management has to develop multiple internal capabilities: an inspirational leadership, a resilient city brand and an ability to learn from other cities through social intelligence. Under the current circumstances, managing finances effectively is becoming an essential enabler, together with managing the city’s projects, performance risks, partnerships, assets and human capital.

Developing a clear vision and internal management capabilities will allow a city to prioritise, invest in and strategically manage, the building blocks or ‘capitals’ needed by any city for long-term prosperity –- social, environmental, cultural, intellectual, infrastructural, ICT and political participation capitals. By putting in place and implementing the appropriate policies, a successful city will maximise its investment in those capitals that are most relevant to its strategic vision, while optimising its investment in those capitals that are less relevant.

All of this should be also be done in a way that is sustainable and through collaboration and partnering with citizens, the private sector, academia and NGOs. This approach is being adopted by visionary cities as a framework to think through the challenges of transformation and to help balance the competing priorities facing city and local government managers.

The future of cities: Tactics that work worldwide

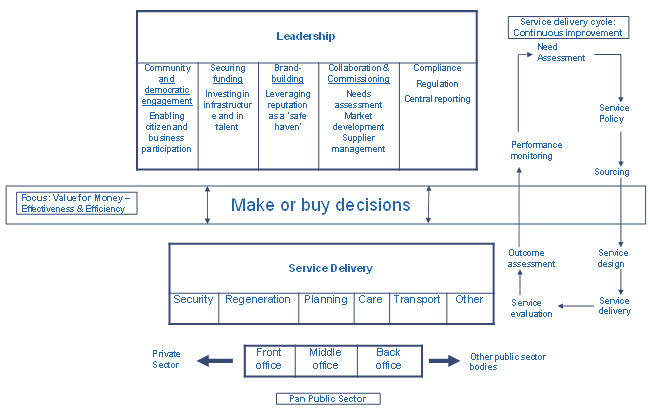

The results of PricewaterhouseCoopers' recent study, "Seizing the day: The impact of the global financial crisis on cities and local public services," demonstrate that local leaders face major challenges not just financially but in terms of building the brands of their localities, engaging and providing leadership for their communities and working collaboratively with an ever growing network of partners, across sectors and geographies, both nationally and internationally.

This requires nothing less than a transformation of local and city-wide management. One new operating model we advocate illustrates at a high level (see chart) the key elements of the operating model for cities and local government, which in turn poses some important strategic issues for local leaders.

Figure 1:A new operating model

A focus on outcomes

For many years and in many cities worldwide, local leaders have responded to often centrally imposed targets and measured their performance against performance indicators which have not always connected to outcomes. In today's world, where the mantra is to do the same with less, a focus on outcomes is critical with the associated cycle of needs assessment, service policy and sourcing, service design and delivery and monitoring and evaluating performance against local outcomes.

Role of commissioning

There are many other services -- cultural ones such as libraries or leisure like parks and community spaces -- where the decision should be made on the grounds of value-for-money and where purchasing the services may represent better value than keeping them within local government.

Where the decision is taken to buy, the role of local government as a strategic commissioner becomes of paramount concern. The skills and capability to procure are not the same as those to commission. The latter requires the ability not only to set up and monitor contracts but to:

•undertake a robust assessment of needs;

•shape and develop the market of providers to supply the services, particularly if this is under-developed in a locality; and

•manage relationships with suppliers to ensure quality is delivered and value for money achieved.

Shared services

Sharing services across organisational boundaries to reduce costs is a concept whose time has also arrived. However, local leaders have the opportunity to go beyond their boundaries and work with others to bring about pan-public sector shared services which really leverage every Yuan spent and ensures the maximum is focused on front-line services.

Increasingly, these services are also not only in the back office like finance, IT and human resources, but in the middle and front office, making use of shared assets and staff to meet multiple needs in the one facility, such as personal advisors navigating individuals across the range of educational, health and social interventions they need to become productive members of society.

To address all of these challenges requires a long term, well managed programme of transformation which in turn will require leadership and determination to see through to conclusion. Given the size of the budgetary challenge, however, there will also be a need for quick wins to go alongside investments which improve performance in the medium to long term whilst also keeping people engaged during a major period of organisational change.

Where it leads

Although cities face different challenges, they can learn from each others' experiences, especially from international good practices, and from the private sector and so better seize future opportunities and face challenges.

To do this, Beijing must adopt a comprehensive approach, starting with a clear vision and supported by the enabling capabilities of leadership, culture and brand. Local leaders must take charge of the situation they will find themselves in and develop a multi-tiered approach so that they can better respond to the challenging global economic and financial conditions that we anticipate in the next 12-18 months.

Beijing government must also look forward and act as intelligent investors. For growth not only to take off but be sustained, government must invest strategically and sustainably in the various ‘capitals’ needed by Beijing for long-term prosperity. Clearly, the priority should be projects with a high social and economic return, particularly in infrastructure, which assist private sector wealth creation. Importantly, cities and local government should be wary of cutting investment plans to balance the books –- this will not solve fiscal deficits, and will only serve to solve today’s problem at the expense of creating new ones for tomorrow.

Of course, Beijing cannot act in isolation and must collaborate both cross-sector and regionally to build ‘joint capitals’ such as intelligent transport systems, as well as across administrative boundaries, to join up critical public services like health and social care.

Most importantly, cities and local governments must continue to rebuild the confidence of the private sector, which is the source of future growth and revenue (through local taxes and charges). There is a need for intelligent and authentic leadership and vision and for policies and mechanisms for collaboration appropriate for today’s globalised economy.

Beijing leaders therefore need to:

•prioritise between core and optional services and ask whether services and activities are needed to fulfil legal obligations, to meet local needs or simply because ‘we’ve always done it this way’ (and could therefore be stopped or done radically differently)

•focus on retaining talent, identifying the critical functions for local government and protecting the talent critical to delivering these functions

•design and develop new service delivery models, particularly commissioning and early intervention and prevention models

•collaborate across agencies, private and voluntary sectors and also spatially, across geographies.

There are also some important implications for central governments which need to:

•provide a stable and sustainable framework within which local leaders have the freedom to invest strategically and sustainably in the various ‘capitals’ needed by their cities for long-term prosperity

•put in place the mechanisms to facilitate collaboration more easily across geographical and administrative boundaries to assist in the creation of ‘joint capitals’.

Finally, for private and voluntary enterprises the challenges are to:

•develop the business case for their investments in local markets by understanding better the implications of the ‘make or buy’ decision and the scale of the potential markets that may be created by the onset of public sector recession at a local level

•build relationships with commissioners and understand better their needs now and in the future; and

•work with local leaders to create a business environment attractive to business.

Beijing leaders must therefore shift gear, from being reactive to events to acting now, with businesses, citizens and central government, to ensure that as the global economy takes off toward growth they are leading the way.

Achieving balance to build the future: A roadmap from the leading global cities

Putting this all into practice, we find the top, world cities are powered into the future by key policies and characteristics, according to Cities of Opportunity, a recent PricewaterhouseCoopers study analyzing 58 separate data variables from 21 leading world cities, including Beijing.

Cities of Opportunity this year takes both a quantitative and qualitative look at the changing picture of city life. And to a great extent, the successes and shortcomings that appear indicate that the more well-balanced a city is for both businesses and residents, the better it will fare.

The study shows that livability is, in fact, an economic asset. For instance, the availability of good housing in cities closely tracks with a city possessing a high standard of living and strong city economy.

Chicago, Stockholm, Sydney, Toronto and Singapore perform well in many quality of life as well as economic indicators, providing both businesses and residents a strong balance. New York, London, Paris and Tokyo may surpass them in breadth and depth of resources, as expected from longstanding world capitals, but pound for pound these “second cities” are proving resilient and attractive to business and citizens.

Stockholm, which enters Cities of Opportunity the same year as being named Green Capital of Europe, comes in first or second in an impressive range of variables including higher education, e-readiness, miles of transit track, congestion management, infant survival, greenness and air quality and R&D spending per capita.

Toronto leads the study in city livability, with high quality of life and health and a diverse population with advanced education. The city works well for business, too, offering strength, good value and, this year, building more skyscrapers than any city except Tokyo.

Chicago builds strong quality of life attributes into its business case. The city comes out on top overall in quality/intensity indicators and finishes in the top tier in areas like mass transit, housing, diversity, number of hospitals and biomedical technology transfer. America’s traditional “second city” (though today third in population behind New York and Los Angeles) also offers strong purchasing power, high air travel volume and other attributes businesses need.

Sydney’s natural strengths and forward-looking policies pull it up from the middle of the pack in power to the second highest score under Chicago when size is removed as a factor. The city scores among the top performers in business, political and quality of life variables ranging from city livability to housing, green space, air quality, congestion management and carbon footprint.

On the other end of the sustainability scale, less well-balanced models for city economies were hurt in the boom and bust. The near-failure of Dubai, not long ago a fast-growing, regional financial capital, is notable. The “miracle in the desert” lacked a resilient, broad base and the city neared bankruptcy in the crisis.

Looking forward after the first financial recovery led by Asia, a number of cities—notably Shanghai, Hong Kong and Singapore—naturally move into the limelight when considering future centres of business, finance and culture. Good cases can be made than any one of them may prove dominant in the Asia-Pacific region and perhaps beyond.

Shanghai, a historic centre of business, finance and culture in mainland China, sits at the fulcrum of what is expected to become the world’s largest economy. The city is well situated to manage China’s domestic capital markets. And Shanghai’s international attraction is signalled by the fact that in this year’s study it ranked highest in foreign direct investment.

Hong Kong keeps a foot well planted in two worlds and in many ways carries a legacy of worldwide trading success into the future. Thirteen years after joining the People’s Republic of China following long lasting British rule, Hong Kong is part of one of the most prosperous nations. For instance, HSBC, one of the world’s largest banking groups, is taking a larger financial stake in China and this year relocates the company’s chief executive to headquarters in Hong Kong.

Singapore makes a strong showing through a range of quality-of-life and business lenses, rising considerably in the power rankings this year and performing well in many quality ones. The city-state is often mentioned when observers speculate on the future financial hub of the Asia-Pacific region with its government retaining a commitment to market security and social order.

Singapore leads Cities of Opportunity's overall ease of doing business indicator. Signalling its global nature, it finishes third highest in number of international tourists behind only London and Hong Kong. Singapore also comes out first or second in shareholder protection and ease of hiring, and also performs well in housing, infant survival, congestion management and lack of crime.

Looking deeper at the cities--A window on Beijing

Dividing the 58 variables into traits of either a city’s raw power or its per capita characteristics, a few cities show greater assets for business, finance and citizens than might be superficially apparent. And they may benefit in growth.

Historically dominant cities long at the heart of the international economy such as New York, London, Tokyo, Paris and Hong Kong predictably lead when power indicators alone are investigated. But “pound for pound,” Chicago, Sydney, Toronto, Stockholm and Singapore display strength for the 21st century on per capita indicators when gauges of power are removed. This indicates they may be poised to move ahead faster than other cities.

For context, power variables used in Cities of Opportunity show absolute size, which ties to historical strength—for instance, a city’s share of top 500 universities. Quality variables normalize cities by population, showing the intensity of a given characteristic. Quality variables are typically per capita ratios that neutralize size as a comparative factor, such as the percent of a city’s population with higher education. Many of them, like congestion management, may also portray an element of a city’s quality in the everyday sense of the word.

Beijing performs well in technology IQ and innovation, giving it a head start in shaping the future. The city ranks highly in this year's study in ICT competitiveness and in mobile phone penetration. As a sign of its increasing economic clout, the Chinese capital also scores near the top in foreign direct capital investment and Global 500 headquarters. Beijing offers additional benefits to companies in terms of demographics, intellectual capital and infrastructure. It boasts a higher percentage of working-age population than any other city in the study; the third most medical schools; and the largest number of hotel rooms (a residual effect of its hosting the 2008 Olympics); and the least expensive public transport.

Beijing's power to attract business ranks fifth overall, behind only London, Paris, New York and Tokyo. Similarly, Beijing comes in fourth in the fast pace of city physical growth in terms of attracting foreign direct investment. In demographics and livability, Beijing scores in the middle of the pack--but its high percentage of working age population and commute time are good.

Housing and city livability pull down Beijing's score--both of which are significant indicators of any city's overall economic health and momentum into the future.

Beijing scores in the lower range in areas including sustainability management, cost, health-safety-and security and ease of doing business, where other major international capitals like London and New York score toward the top.

To move up, Beijing can look at the policies of some leading cities.

Balancing quality and power

Long-established capitals New York, London, Tokyo and Paris retain their towering advantages. And none are resting on their laurels. New York and London, numbers one and two in the power ranking, also rate highly on quality variables that require forward-looking policies and actions. Number three on power, Tokyo performs at the top of health and medical care variables, befitting the centre of Japan where the average lifespan of 83 years leads the world. The City of Light, Paris, remains just so in many complementary ways—rating in the top two in gauges of education, green policies and the scope of entertainment, embassies and fashion.

In terms of any comparison to other fast-growing Asian cities, many are positioned well to move to the forefront of the region and in future the forefront of the world if progress continues on the same booming path that powered the region out of the global recession before the rest of the world (as above).

But looking at the leaders across the world and the traits that are moving them ahead, Chicago stands tall in many areas. Among them are Chicago’s role in finance and business; mass transit and congestion management; diversity; purchasing power; and in many of the key quality of life indicators. Much of the city's old “bareheaded, shoveling” industrial grit has also gone green thanks to continuing attention to the city’s legacy of grand parks and architecture. The Chicago Climate Exchange, first active carbon emissions trading platform in the US, symbolizes the emerging city just as aptly as the commodity futures trading pits for pork bellies and corn do its heritage.

Chicago slips four rungs in power rankings this year in the study. One reason is that Chicago, like Beijing in China, is just one of many big and attractive US cities vying for foreign investment, and this year a second variable has been added to measure foreign direct capital investment in addition to last year’s variable—job-creating greenfield investment.

The quality rankings also place Sydney, Toronto, Stockholm and Singapore tightly bunched in the top tier of cities. Sydney’s natural strengths and forward-looking policies pull it up from the middle of the pack in power to the second highest scoring city when size is removed as a factor. The scenic Australian port scores among the top few cities for its business, political and quality of life indicators ranging from city livability, to housing, green space, air quality, congestion management and carbon footprint.

Toronto and Stockholm, two northerly cities at arm’s length from the madding crowd if not as distant as Sydney, both offer business and citizens good reasons to brave the long, cold winters.

Toronto tops city livability, offering high quality of life and health and a diverse population with advanced education. In addition, the city offers strength (scoring highly this year in skyscraper construction) and good value for business. Toronto benefits from a Canadian immigration policy aimed at attracting highly skilled workers. All this should help Toronto to continue prospering in a globalized world.

Stockholm, new to Cities of Opportunity this year, has long been called the Venice of the North. In fact, built on an archipelago of islands, the city glitters not only because of its lacework of waterways and nearly midnight sun in summer. Many of the study’s variables reflect Stockholm’s strengths. Relatively small in size, the Swedish capital ranks first or second in: higher education, e-readiness, miles of transit track, congestion management, infant survival, greenness and air quality and R&D spending per capita.

Stockholm's planning for a sustainable future, for instance, has been a constant throughout city governments for nearly 60 years--well ahead of other cities and continuing no matter what political party held power in Sweden and the city. Today, Stockholm boasts cleaner air and less traffic congestion than years earlier.

Singapore, too, makes a strong showing in many ways. Judged in the power rankings, Singapore jumps three spots from last year overall and tops all cities on ease of entry. Singapore’s international tourist flow (including both business and pleasure travel) is only exceeded by London and Hong Kong. In normalized variables, Singapore comes out first or second in shareholder protection, ease of hiring, housing, infant survival, congestion management, flexibility of travel and lack of crime. The city-state leads the study in ease of doing business.

Frankfurt, another small city, makes the top tier when normalized by population based on a strong economic base and forward-looking urban policies. The city sits at or near the top in variables ranking higher education, financial services employment, strength of currency, purchasing power, political and social environment, miles of mass transit track, commute time, housing, recycling and city livability.

Focus on innovation

Innovation is a pillar of any city's future when it comes to building new companies, industries, jobs, wealth and resources. And this innovative power adds a final important piece to the puzzle.

An eye on tax policy

In terms of tax policies, overall PricewaterhouseCoopers observes in its recent report, Innovation--Government's many roles in fostering innovation -- that most countries and cities have been adding new tax vehicles to support modernization and innovation. This applies across both emerging and developed economies.

Two trends are motivating this greater tax friendliness toward innovative activity in the private sector. One trend stems from reduced barriers to trade across countries and regions. In a more globalized economy, the balance of power between buyers and sellers of goods and services has been shifting to buyers—especially in economies that were formerly closed to foreign goods and services. The second motivating trend is that emerging economies have pursued manufacturing opportunities, offering low-cost labor pools as a compelling alternative for multinational corporations. That contributes to lower costs and thus lower prices over time for most manufactured goods.

The combined effect of these trends has been the inability of manufacturers to maintain high profit margins for products that lack any distinctive, proprietary, or value-added innovations. As a result, innovation that addresses customer priorities has become a more important driver of economic growth for all countries and cities, emerging and mature. Because these trends show no sign of reversing, governments are likely to continue pursuing tax policies that foster innovation.

Countries and cities that have been successful at fostering innovation have tended to build a tax platform that includes a number of elements for corporate owners and investors: low taxes (through an overall low tax rate, industry-specific low tax rates, or tax holidays); a regime of R&D tax incentives such as credits and/or deductions; an intellectual property/royalty payments (IP) tax regime; incentives for capital investment such as investment tax credits; and a holding company regime. In addition, these countries also focus on the investor side of taxes by, for instance, giving the investors tax breaks.

Certain tax incentives tend to be more effective at particular stages of an economy’s development. In the early-emerging stage, when modernization of the business base is a top priority, useful tax incentives tend to focus more on capital expenditure and less on boosting profits. In the later-emerging phase, fostering innovation stands as a top priority, and the tax focus moves to R&D tax credits. (To help start-ups or companies with early-stage losses, these credits can be made refundable; that is, the company gets cash in hand.) In the mature phase, governments generally want to exploit the innovative activities that have been put in place, so they focus taxes more on the output of R&D, as well as keeping it in country. IP regimes and “patent box” regimes, which lower tax rates on income from patents, are common here.

Public and private innovation: Creating the right climate

When considering the processes by which an economy sponsors and facilitates innovation, it’s important to clarify the sources of funding for innovative activities and the motivations for funding.

Directed funding from the government typically aims to serve broader social, political, or national defence purposes. Consider the US goal, in the 1960s, of safely landing a man on the moon and returning to Earth. Success was measured against that goal, and although many hundreds of large and small innovations emerged from the effort; there was no consideration by the US government of their commercial viability.

By contrast, private innovations are driven by market competition and must return a profit on their investment costs in order to be considered successful. Companies launch many innovations, most fail, and a few prove commercially successful.

This distinction between directed and market-based innovation is critical when considering the role of government, particularly in the domain of tax initiatives. The logic behind tax incentives is to change the risk/reward calculations of market participants in order to encourage them to invest more in research, product development, and business process improvements (often supported by software). Implicit is the assumption of a functioning marketplace–multiple buyers and sellers participating in transactions without undue external influences unrelated to the value being exchanged. If markets are insufficiently developed–say, if a single large seller dominates–there will be no risk/reward calculation to promote innovation, and tax incentives will become irrelevant.

Governments thus have been most effective when they acknowledge the status of their existing markets and take steps appropriate to their individual situations. If a country’s markets are insufficiently developed, the government can encourage new entrants through grants, loans, and looser policies regarding foreign participants. It can ensure that courts enforce business contracts and take other steps that make market systems more predictable and stable. With a functioning market in place, tax incentives are more likely to have their intended effects on innovation.

How Technology and Innovation Interact

Technology and innovation are closely intertwined. Each can help to drive productivity growth, by improving business processes and organizational effectiveness. Each can lead to new products and services, some of which will succeed and generate income growth, as well as benefit society. They reinforce each other by increasing the speed and flexibility of new business models.

Cities and countries with a strong technology infrastructure (personal computer ownership, broadband and mobile phone penetration, degree of Internet security, and so on) are better positioned to innovate in business, especially in tech-based sectors. According to a study of 120 countries by the World Bank, for every 10% rise in broadband penetration, there is a 1.3% rise in GDP.

Conclusions for Beijing

Beijing's efforts to build a leading world city will extend directly from its ability to seize the tremendous advantages it possesses, respond to the challenges in its way and, ultimately, balance the two with a holistic perspective on the issues that make a city successful in the 21st century -- the key financial, intellectual, social, environmental, technical, infrastructural and political capitals that great cities.

主办:中国国际贸易促进委员会北京市分会

建设运维:北京市贸促会信息中心

京ICP证12017809号-3 | 京公网安备100102000689-3号